Systematic Investment Plan (SIPs) are touted as the best option to increase your wealth and achieve your goals. But how exactly do they help you?

In our last blog, we explained how mutual funds work and what are the types of mutual funds that are available in the market. In today’s blog, we will be explaining what SIPs are and why you should invest in mutual funds via SIP.

You can see the advertisements of mutual funds and SIPs almost everywhere these days as they are a popular choice among retail investors in India. According to the Association of Mutual Funds in India (AMFI), the Indian mutual fund industry has 5.17 crore SIP accounts through which investors regularly invest in Indian mutual fund schemes. Also, the total amount collected through SIP during February was 11,438 crore.

Everyone is raving about it and loving it. So, here is our article, explaining everything about them in easy-to-understand words. No jargon will be used and that’s the Koshex promise!

What Is A Systematic Investment Plan?

A Systematic Investment Plan (SIP) is a plan that allows investors to make regular, equal payments to a mutual fund scheme. If you choose to invest ₹3,000 in an equity mutual fund scheme every month via SIP, then that amount will be deducted automatically from your bank account on the date of your choosing. Just like how Recurring Deposits (RDs) deduct money from your bank account in regular intervals, SIPs do the same.

How Do They Work?

Let’s say that you start investing ₹10,000 every month and this investment would create units in the mutual fund based on the NAV (Net Asset Value). If the NAV is 25, then 400 units would be allotted (10,000/25=400).

The NAV is the reflection of the market movement on which the fund is based and it can go up or down based on how the market functions. If the stock market trades lower, you would be allocated more than 400 units and vice versa. However, the amount you pay (i.e. ₹10,000) will remain the same even if you are allocated over 400 units or less than 400 units per month.

| Month | NAV | SIP Amount | Units Allotted | Cumulative Units |

| January | 25.0 | 10,000 | 400 | 400 |

| February | 26.3 | 10,000 | 380 | 780 |

| March | 24.3 | 10,000 | 410 | 1,190 |

| April | 28.5 | 10,000 | 350 | 1,540 |

| May | 22.7 | 10,000 | 440 | 1,980 |

When you examine the example closely, you can see that when the NAV is high (likely when the market is up), the number of units allotted for the same ₹10,000 SIP is lower compared to the month when the NAV is low (market is down). Over time, as your SIP progresses, you will have invested across all market phases. So, your average cost will be reasonable. This is called rupee cost averaging.

Benefits Of Investing Via SIP

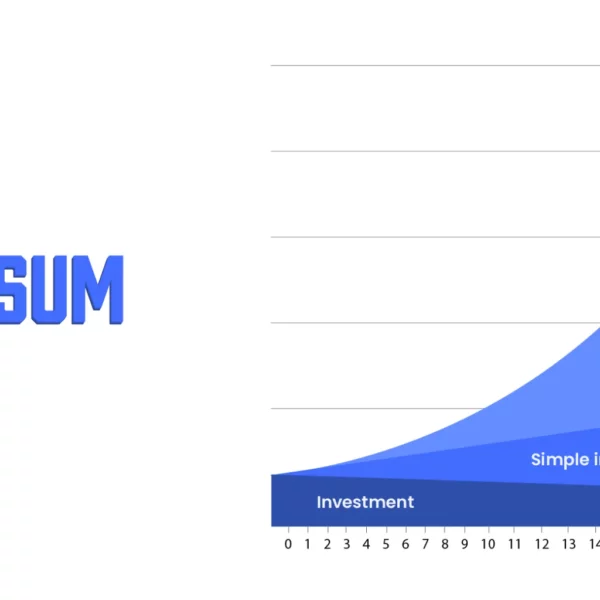

Apart from Rupee Cost Averaging, the biggest benefit of investing via SIP is the power of compounding. The interest you earn on your accrued interest is referred to as the power of compounding. In other words, it means reinvesting the earnings you get from your initial invested amount instead of spending it elsewhere.

For example, if you invest ₹10,000 with 8% interest every year, then your principal amount is ₹10,000 and the earnings, at the end of the year, are ₹800 (8% of 10,000). However, in SIPs, the interest is reinvested, hence your principal amount for the next year becomes ₹10,800 (10,000+800) and the earnings you get are ₹864, which is ₹64 more compared to the first year. Even though this looks like a small amount, it can make a huge difference to your investments over a long term.

| Simple Interest | Power Of Compounding | |||

| Year | Principal Amount | Interest earned (at 12% per annum) | Principal Amount | Interest earned (at 12% per annum) |

| 1 | 10,000 | 1,200 | 10,000 | 1,200 |

| 2 | 10,000 | 1,200 | 11,200 | 1,344 |

| 3 | 10,000 | 1,200 | 12,544 | 1,505 |

| 4 | 10,000 | 1,200 | 14,049 | 1,685 |

| 5 | 10,000 | 1,200 | 15,735 | 1,888 |

| Total interest earned | 6,000 | Total interest earned | 7,622 | |

| Total value of investment | 56,000 | Total value of investment | 71,150 |

You can see how the power of compounding helps you increase your investment value over the long-term. When it comes to the power of compounding, the more you invest at a young age, the more your money will work for you over time and the sooner you will be able to build a sizable corpus to help achieve your financial goals.

Types Of Systematic Investment Plan (SIP) To Choose From

1. Regular SIP

This is one of the popular SIP investment routes. In a regular SIP, you can fix your investment amount and investment interval. The fixed amount will be deducted automatically at the given time.

2. Flexible SIP

In this type, you can adjust your SIP amount based on income, expenses and market conditions. You can even set this SIP to automatically invest more when the market declines and less when the market goes up.

3. Step-up SIP

Here, you can set up your investments to increase by a small amount periodically. Let’s say, you set up an SIP to invest ₹5,000 in January, you can increase the amount by ₹1,000 every subsequent month. You can also ask the fund house to increase it by ₹5,000 after every 12 months.

4. Perpetual SIP

In a regular SIP, you can choose the start and end date of your SIP. However, in a perpetual SIP, your SIP will continue until you indicate to the fund house to discontinue it.

5. Trigger SIP

In this type, you can set up your SIPs to be triggered if the NAV equals a certain value. With this type, you may even trigger your SIP based on the values of popular benchmark indices like Sensex and Nifty.

Bottomline

There are so many options available within SIP and they are preferred by many as it makes one a disciplined investor. It also helps you get your finances on track, stick with your budget, and think twice before splurging on unnecessary things.

Convinced about the benefits of SIP? Head over to Koshex and choose from over 10,000 mutual fund schemes. You can choose the scheme that suits your financial needs and future goals and invest via SIP. Trust us, life is better when you have a solid financial plan and it is better with SIPs!

Tell us in the comments below if you are investing via SIPs or are interested in starting the journey.

Leave a Comment